"Invest for the long term" is a trap

A rationalization for accepting risk and volatility

Listen or watch instead:

Podcast →

YouTube →

“Invest for the long term to get a ‘high’ average return” is kind of like a golden rule of Wall Street. And while investing for the long term and compounding for the long term can be good, with conventional investing, because of the volatility and risk, you must invest for the long term - or it doesn’t work. So it really ends up being nothing more than a justification. It’s an excuse to cover for the volatility and risk you’re taking on by buying into the stock market.

Locked in Regardless

With the conventional approach, you end up locking your money away and subjecting it to all the market volatility for decades. You either hard-lock your money away, in the case of a 401k or IRA, where you can’t get to it without paying taxes and penalties, or you lock it away in a regular brokerage account, because you can’t get to it without interrupting that averaging effect that “protects” you from market volatility. So you’re locking it away regardless. You have to keep it there. Otherwise, the average rate-of-return story falls apart.

And because of that, your money can really only do one thing at a time.

Think about what that means when you hit a financial bump in the road (which will happen): Job loss, a medical emergency, car or home repairs. Or on the opportunity side: an investment, starting a business, a career change. For example, when I changed careers from tech to financial services, I was only able to do that because I had a bunch of money saved. A lot of it in whole life insurance. I used policy loans to help pay the bills while getting started, and throughout, I never lost the growth of my whole life insurance cash value. If that money had been in a 401 (k), I couldn’t have gotten to it without paying taxes and penalties, and then losing the growth on it forever. Same with a brokerage account, less the penalties. You lose the use of your money in the near term in the hope of something good happening over the long term. And you have no idea whether or not that’s actually going to happen.

The Four Rules of Financial Institutions

The following clarifies why conventional advice is structured the way it is. Financial institutions have four rules:

They want us to contribute money to them.

And contribute money on an ongoing basis.

Then hold onto that money for as long as possible.

And distribute that money back to us in a limited manner.

Just look at your 401(k), and you'll know this is true.

When we put money into the stock market, or even worse, into 401 (k) s and other qualified plans, we are completely giving up control over our capital, and we have no idea what’s going to happen with it. We don’t know how much we’ll be able to contribute over the years. We don’t know what it’s going to grow to. We don’t know how much we’ll need in retirement. We have no idea what the taxes will be by the time we have to pay them, after deferring for decades. And so we don’t even know how much we can get later when we want or need it.

We’re entering into this agreement, where we’re taking all the risk and providing all the capital for nothing that we can count on in return. We’re trading all of that for a complete unknown.

What exactly about that is a “financial plan?”

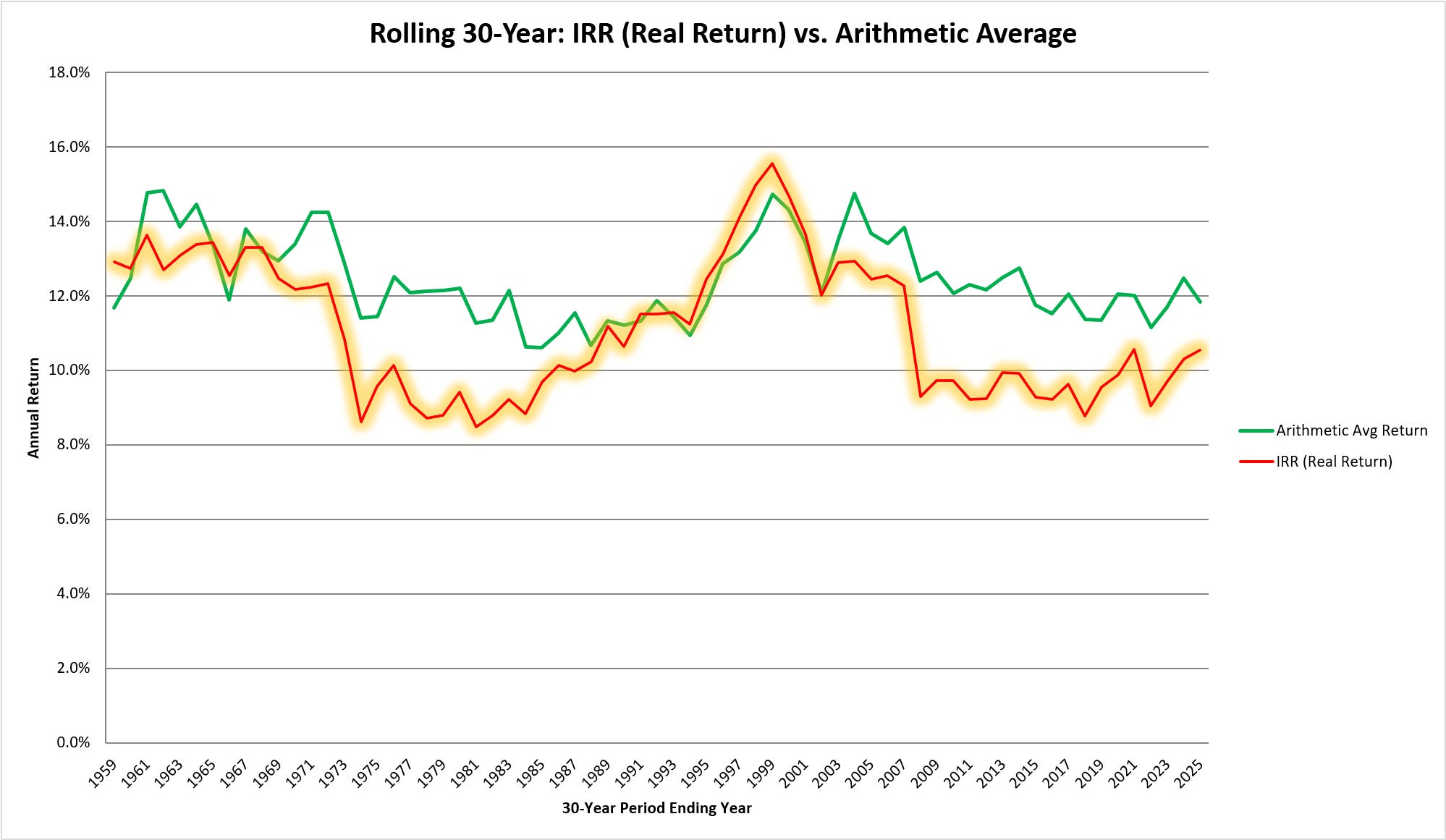

Average Rates of Return: A Made-Up Metric

If you just invest for the long term, they say you’ll get whatever they’re saying these days, a 10, 12% average rate of return. They say this like it’s a foregone conclusion, and, unfortunately, there are really a lot of problems with this assumption.

The average return is simply the arithmetic average of the actual rates themselves. This calculation doesn’t have anything to do with the return you’ll actually get. If you go back and look at the entire history of the S&P 500 and look at rolling 30-year periods (1930 to 1959, 1931 to 1960, and so on), there are 67 thirty-year periods. The real return over any of those periods is significantly less than the average return 75% of the time.

And I’m not talking about just a little bit here. On average, it’s about 1.35% per year difference. Investing just $10,000/yr, this difference adds up to millions of dollars at the end of 30 years.

This is a real problem that a lot of people aren’t aware of. They’re just told they’ll get an average return of, say, 12%, but those numbers are completely made-up. Not only are they made-up numbers, but the made-up numbers are all based on past performance we know, with close to 100% certainty, will never happen again in exactly the same way. So the data is meaningless in terms of what’s actually going to happen with your money.

The Long Term Eventually Becomes the Short Term

There have been 10 and 20-year periods where you can have no growth or even lose money. We need to become aware of this because the long term eventually becomes the short term. As you approach retirement or need the money, that timeline becomes now. This is where sequence of returns risk comes in.

The conventional “invest-for-the-long-term” approach is really kind of a trap, because it demands that you do it. It’s required to overcome the volatility. But the real problem is that it doesn’t even solve the volatility problem! People invest for the long term, and then the dot-com bubble happens. Then 2008 happens. And it really, really matters when they happen.

If you’re retired and pulling money out to get income, and the market goes down, your income needs don’t typically change. So you have to sell more shares to get the income you need. Cannibalizing these shares, so to speak, makes it so that your account can never bounce back, even when the market goes back up. You can do all the best long-term investing that you want, and if 2008 hits you the year after you retire, well, that’s a problem. 40% of your money is gone in year 1 of your retirement. Not good.

And the thing is, we only get one shot at setting ourselves up for the later years. There are no do-overs!

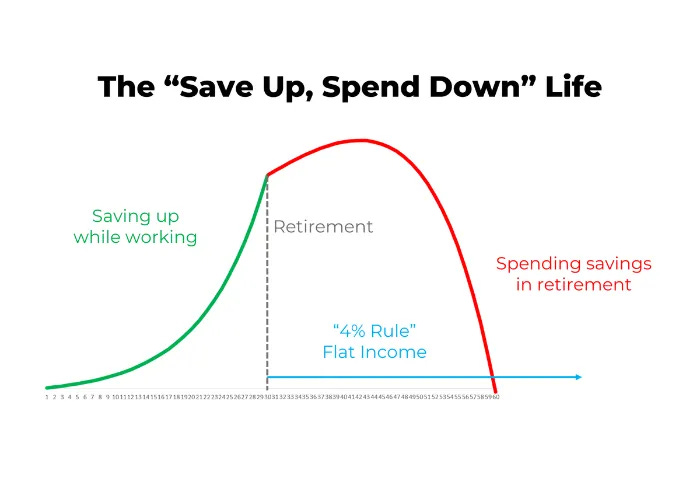

The Save-Up, Spend-Down Life

Because everyone is only thinking about the accumulation phase of their life and locks themselves into just trying to create the “biggest account,” what ends up happening is we end up living what I call the save-up, spend-down lifestyle.

We give up control of our money, try to save as much as possible, but have no idea what will actually happen to it. So we’re in a constant state of worry over what the markets will do and how it’ll affect our plans. And then when we get to retirement, we spend it down. Maybe our heirs get a little bit. Our kids might get something, grandkids, but it’s always whatever’s left over. Our financial lives end up mostly just being about us. And that’s sad. It’s no wonder so many people are trying to make ends meet. It’s because our plans suck and they’re only designed for a single generation.

Not only that, but how many things have to go wrong for the save-up, spend-down strategy not to work? Really just one thing. If one thing goes wrong, it can blow the whole thing up. Which means, how many things have to go right? Everything has to go right in order for the typical plan to work out for us.

Everyone, in theory, knows we should plan for the worst-case scenario. But in practice, when it comes to our finances, everyone is planning for the best-case scenario — those 10, 12% average returns — based on historical market data that will never be repeated exactly again.

What Thinking Long Term Actually Looks Like

True long-term thinking requires a foundation that works in the short term as well. With the Infinite Banking Concept, we’re planning for 70 years, minimum. Whole life insurance policies go to age 121 and then are passed along to the next generation, guaranteed, on an income-tax-free basis. We’re planning for generations, but in our format, we are still maintaining control and liquidity today. This gives us the ability to navigate all the bumps in the road, roll with the punches, and take advantage of opportunities that come along, rather than only hoping to get whatever rate of return we end up getting in a market-based account.

Whole life insurance is a special, cash-equivalent asset that gets better every single year, no matter what happens in the market. It’s guaranteed to only go up, never down. Designed for the ultra-long term, and yet it provides liquidity when needed today, no questions asked. You can use the money for emergencies or opportunities, and it does not interrupt the compound growth on the cash value and the death benefit.

This is a key concept: uninterrupted compounding.

With Infinite Banking, you can use money in the short term via policy loans without sacrificing the long-term growth. The underlying cash value continues to compound as if you never touched it — because you didn’t. You borrowed money from the insurance company, collateralized by your cash value.

This is just leverage, which every investor is familiar with. And there is no safer and easier way to get leverage than with whole life insurance.

I have a client who was using margin to do other investments, and he faced margin calls and liquidity crunches because his money was tied up in the market. That’s one of the reasons he implemented IBC - to ensure he had a capital base that was not subject to market whims.

And here’s what we can do with policy loans. We can go buy an investment — real estate, commercial notes, starting a business, whatever it is. And when you pay that loan back, the whole life insurance grew the entire time. We’re giving multiple jobs to every dollar in our ecosystem.

This is why life insurance is sometimes called the “and” asset. You don’t have to choose between short-term access and long-term growth. The Infinite Banking Concept is the process, whole life insurance is the product, and together they allow us to have both.

You capitalize first (which is just a fancy way of saying saving money), which is long-term thinking. And then you use a policy loan to deploy that capital, to do all your investing. That’s what creates the growth. We use whole life insurance as our cash asset, and we use policy loans to deploy capital. The idea isn’t to get a high return inside the whole life insurance policy; the idea is to get a respectable return (better than anything else you could put it into that’s a cash equivalent) and then use that cash to create your higher returns outside the policy.

With whole life, we have a foundation that does five, six, seven jobs, or more. Liquidity through cash value. Guarantees. The death benefit, if the worst were to happen. Chronic illness and terminal illness protection through the accelerated death benefit riders. Creditor protection. No volatility. And built-in retirement and estate planning strategies.

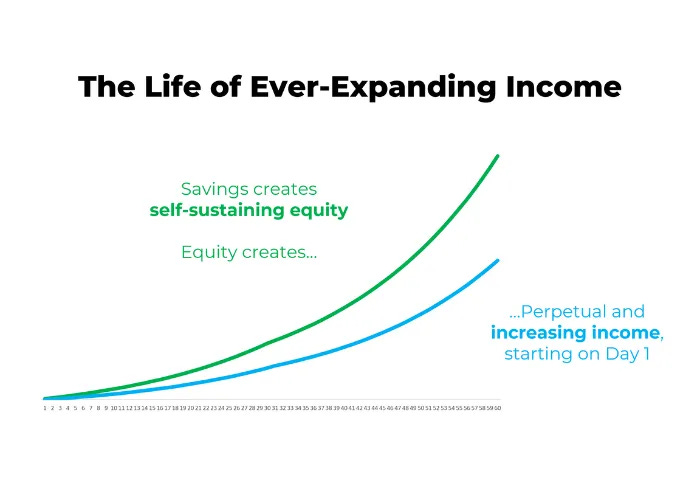

A Life of Ever-Expanding Income

The best planners out there are planning decades in advance. They’re not planning just for themselves — they’re planning for their kids and their grandkids and their great-grandkids. And with the Infinite Banking Concept, we can make those plans and still have access and liquidity today to handle all the things we don’t know are coming around the bend.

I try to talk to people about what I call the life of ever-expanding income.

If you capitalize first with whole life insurance, then use policy loans to buy income-generating assets, by the time you get to retirement, you’ll probably have so much income coming in from outside sources — other than your job — that you won’t even need to spend anything down. You’ll just have income. And you’ll probably have more income than you could ever get by spending down your account.

Don’t let investing for the long term be an excuse for losing control of your money. You’ll never be in a worse position by having access to cash.

Think long term. Plan generationally. But never give up control in the process.

To learn more about how IBC might apply to your situation, schedule a free consultation at StackedLife.com.